All Categories

Featured

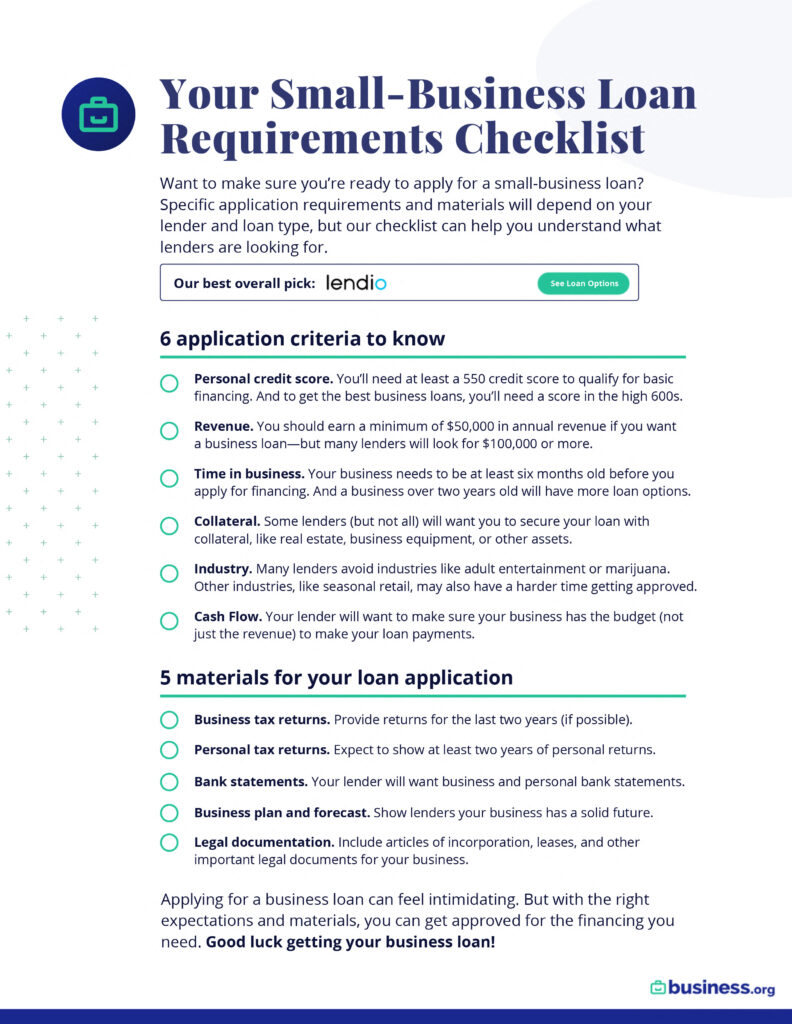

In Texas, as with anywhere else, demonstrating both a solid company foundation and monetary reliability is essential. The plan must likewise present extensive, as well as forecasts that detail how the loan will be used as to achieve particular development objectives.

In addition, lending institutions will evaluate previous and forecasted to guarantee sufficient after loan dispensations. Businesses must prepare to reveal how they plan to service the debt through clearly articulated and usage of funds.

often deal with special difficulties in protecting funding due to an absence of functional history and financial records. For these business, consisting of those led by and those in, traditional bank loans may not be a feasible option. Alternative funding such as or can provide more available opportunities. They may offer smaller amounts of capital that can be vital for preliminary costs like inventory and working capital.

Cutting Costs Through Operational Automation in Modern Storefronts: Typically ranging from $10,000 to $50,000, to cover startup costs.: May exchange equity for capital, focusing on appealing startups.: Permits businesses to raise small amounts of money from numerous backers. frequently have a performance history which can assist in access to extra funding types such as or bigger term loans.

The Benefits of Cloud Store Accounting

Choices like offer a variety of terms ideal for recognized organizations, with APRs that can be competitive. Additionally, some organizations use programs designed to offer quick financing with low rates to help keep working capital, supporting businesses poised for expansion.: Loans of $10,000 to $1,000,000+, providing a lump amount for larger investments.

: Customized loans created specifically for acquiring organization devices. As soon as a small company in Texas protects a loan, prioritizing monetary management is essential to guarantee smooth payment and efficient usage of the funds for purposes like business expansion, payroll, and purchasing devices. It is vital for organizations to preserve to handle effectively.

Securing capital is an essential decision for little services. The best loan at the ideal time can fund growth, cover cash ow spaces, purchase devices, or safe residential or commercial property. The incorrect one can be damaging. In 2026, little services in Florida and Georgia will have more providing choices than ever, including SBA loans, term loans, credit lines, business property nancing, and devices nancing.

This guide outlines offered loan types, SBA program specics, how cooperative credit union compare to banks, credit history benchmarks, documents, rejection aspects, and specialized property/equipment and vehicle loans. Each section oers a foundational understanding before fulfilling a lender.iTHINK Financial oers small company owners in Florida and Georgia a range of obtaining alternatives developed to match their growth cycle from SBA and term loans to credit lines, business realty nancing, and automobile and devices loans.

Will the Workflows Scale in 2026?

Explore service lending at iTHINK Financial. Access to capital is a critical organization choice that forms money ow and development.

Cutting Costs Through Operational Automation in Modern StorefrontsThey are best for handling cash flow spaces or unanticipated expenses. SBA loans are government-backed and released by approved loan providers (SBA 7(a) loans prevail). The SBA guarantee decreases loan provider risk, typically offering better, longer terms for a vast array of uses, from property to working capital. Industrial genuine estate loans are for acquiring, building, or refurbishing owner-occupied business property, underwritten based upon the company's income potential.

Comprehending typical loan sizes helps organization owners calibrate their expectations before using. The approximated U.S. bank loan market was valued at over $1.4 trillion since early 2026, and throughout authorized borrowers, small companies got approximately 75% of the financing quantity they asked for. Loan amounts differ commonly by product and loan provider, however most of small company owners look for amounts under $500,000, putting traditional term loans, SBA 7(a) items, and cooperative credit union nancing well within reach for a lot of candidates.

The SBA ensures a part of loans from authorized lenders, motivating them to nance companies that might not certify for conventional loans. Organization owners can use profits for real estate purchase or renance, business acquisition or start-up costs, equipment purchases, stock, buildouts, and working capital.

{kind=link}

Latest Posts

Modern Team Scheduling to Higher Efficiency

Essential SME Accounting Tips for Boost Capital

Combining Automation and Boost Store Fiscal Sustainability